History rhymes and often repeats

History rhymes and often repeats

Key topics discussed today include:

New extremes – The long end of the yield curve has extended last week’s decline, which spells trouble for the US economy

The calm before the storm – While the S&P 500 Index has consolidated with VIX heading down, things look to reverse as we near the January reporting period; another selloff to come

Pivot ahead – JP Morgan expects a disinflationary environment to emerge from Fed’s QT, a strong US dollar, wage growth declines, and a softening housing market which should prompt the Fed to pivot by end of 2023

Valuation is an art – JP Morgan sees corporate sentiment falling as revenue and profit margin forecasts come down; S&P 500 still looking expensive

Will the cap work? – European Union decides on a price cap for Russian crude oil and requires backing; oil prices set to reverse to the upside as China reopens

Not over till it’s over – Slew of banks comment on Tuesday’s RBA announcement of rate hikes; 25 bps likely for December, but more to come

Early Christmas – Soaring coal prices will place Australia’s budget bottom line in balance, albeit temporarily

Light at the end of the tunnel – Cities in China are easing restrictions with officials ramping up vaccination for the elderly and immunocompromised

Notable stocks and indices mentioned include the S&P 500 Index, the US Yield Curve, the VIX Index, WTI Crude Oil, Apple, Peloton, Premier Investments, Chalice Mining, Haidilao, and SSP Group

Good morning,

Wall Street had a mixed day on Friday, with the benchmark indices closing off their intraday lows on Friday. The November payrolls report came in stronger than expectations with unemployment unchanged at 3.7%, which caused initial weakness on concerns the Fed will be forced to keep tightening, but the bond market flashed a different signal with long duration yields falling sharply. The dollar index was little changed, gold futures dipped about 0.2% to $1,812 an ounce and West Texas Intermediate oil dipped more than 1% to about $80 a barrel.

The Dow Jones rose 0.1%, the S&P 500 lost 0.12%, to 4,071 and the Nasdaq Composite dropped 0.18%. Pertinently, volatility continued to fall with the VIX breaking below key support at 20 in a sign that the rebound rally on the SPX is holding above the key downtrend trendline resistance which points to further topside extension over the coming week.

S&P 500

Market focus has now shifted to the upcoming Federal Open Market Committee meeting which is set for December 13th/14th next week. Following Fed Chair Powell’s speech last week, I don’t expect any deviation to the current rate tightening path and even with the strong employment data on Friday, a rate hike of 50 bps seems all but a foregone conclusion.

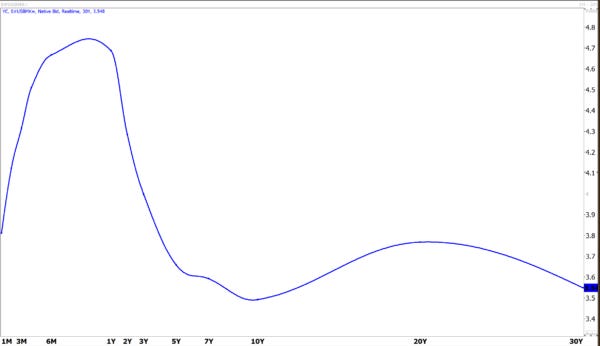

While the 2 year bond yield rose 4 bps to 4.21% on the strong jobs data, the long end of the curve extended last week’s decline which is a sign of trouble ahead for the US economy. The US yield curve is steeply inverted which seldom in history has seen the economy avoid a recession.

The US yield curve inversion has steepened with short end rates well above the long end of the curve. The US economy has seldom in history avoided recession when the curve has been this inverted. History is therefore set to “rhyme if not repeat” on this front next year.

US yield curve

I think the rally can further extend higher over coming weeks, given the technical setup. The SPX is continuing to consolidate after staging a breakout above bear market resistance a few weeks ago. Positioning is low, sentiment has improved but still remains poor, while sidelined cash and liquidity levels are abundant. The short interest came in last week, but we could still see further covering as positions are closed out in coming weeks.

Retail investors which have remained notable sellers since October could reverse to the buyside and this might sustain the rally for several more weeks yet, until we get closer to the December reporting season where market focus is likely to shift. Looking ahead, equity market volatility, as measured by the VIX, broke down below key support at the key 20 level falling 3.9% to 19 on Friday which is the lowest level since just prior to the Ukraine war.

Further selling pressure might push the VIX down towards 16/17 in coming weeks which would lend support to the ‘risk on’ rally. However, I don’t expect the VIX to remain subdued for too much longer with the December quarterly reporting period likely to induce a further equity market selloff, as investors question where earnings and valuation are headed – with the SPX now priced once again on an expensive forward PE of circa 19X.

Vix index

This is a view from investment bank JP Morgan, which pivoted from a bullish outlook for stocks long held throughout most of the year. JPM now expects US equities to drop through the first half of 2023, as “the Federal Reserve continues an aggressive fight to dampen inflation”, then stage a rebound as the central bank changes tone later in the year.

JPM expects the S&P 500 to retest this year’s lows at 3500 as the Fed “overtightens the US economy amid weaker fundamentals”. Mr Dubravko Lakos-Bujas, Chief US equity strategist at JPMorgan wrote in a note on Thursday that “fundamentals will likely deteriorate as financial conditions continue to tighten and monetary policy turns even more restrictive (Fed raises rates by another 75-100bp with an additional ~$1T in QT), while the economy enters a mild recession with the labour market contracting and unemployment rate rising to ~5%.”

Mr Lakos-Bujas believes that after any potential sell-off, disinflation, rising unemployment, and weaker corporate sentiment should prompt the Fed to signal a pivot that lifts the S&P 500 to 4,200 by the end of 2023.

JP Morgan is in the falling inflation camp (which I believe is already playing out in markets, hence the fall in long duration bond yields and a steepening in the curve) expecting “a disinflationary environment to emerge from the Fed’s quantitative tightening, a strong US dollar, significant wages growth declines, and a softening housing market. Meanwhile, unemployment levels will rise due to the higher cost of capital from interest rate hikes, while the US enters a mild recession next year.”

JPM also sees corporate sentiment falling, as forecasts for revenues and profit margins come down, forecasting a drop in 2023 S&P 500 EPS forecasts to $205 from $225 on “restrictive monetary policy, evaporating consumer savings, and elevated geopolitical risks.” If earnings come down this quickly and hit the JPM target, then the SPX is priced on a forward multiple of 20X.

Valuation is even more stretched when applying Morgan Stanley’s projected earnings of $195. The bottom-line, is that investment banks are lining up behind a call for dramatically lower earnings for the S&P 500 companies next year and so it stands to reason that it is only a matter of time before Wall Street analysts commence lowering CY23 earnings dramatically in the months ahead. While investor FOMO could soon begin to see investors chase the rally, the best path forward in my view is to stay disciplined and maintain readiness to deploy cash around March next year.

US equities command a much higher valuation than the rest of the world, so it’s logical for the downside risk reward skew for the S&P 500 to fall harder than other markets. But I expect the final bear market selloff phase in the SPX to impact most equity markets, albeit ‘peak to trough’ percentage losses could well be likely milder and less severe.

Moving onto crude oil markets, the European Union has decided on a $60-per-barrel price cap for Russian crude oil and will now require member nations as well as the G7 group of countries to back the plan. The price limit, if finalized, would take effect from December 5. The Russian Urals benchmark last week traded at $66.54 a barrel which is a large discount to Brent Crude at $85.57, and WTI crude at $79.98.

The EU’s objective is to cap the price of Russia’s oil to curb the country’s $100 billion annual revenues from energy exports, and undermine the principle source of funding for the war in Ukraine. For the cap to work, a “buy in” is needed from all 27 member nations as well as the major economies in the world including Canada and Japan. India and China have been notable dissenters and both countries continue to support Russia with direct importations.

With Shanghai easing some Covid restrictions and move towards reopening the economy in the first or second quarter of next year, global aggregate demand is going to reassert. This could see oil prices reverse to the upside and this will place the cap at risk of collapsing in my view. Nations faced with high inflation are going to be compelled to secure energy from whatever source is available, including Russia.

OPEC met over the weekend and agreed to stay the course on output policy ahead of the pending price cap and ban on Russian crude. OPEC+ will adhere to their plan of reducing oil production by 2 million barrels per day, or about 2% of world demand, from November until the end of 2023. For now, the cartel will avoid any further price supporting cuts to production, but this could change if the EU cap fails to work, and oil weakens further towards $70.

The lower US dollar has provided some relief, and this is pointing to a technical ‘double bottom’ pattern forming on the charts. However, I would give the energy market bears the benefit of the doubt and would avoid buying or chasing energy equities at present. Energy stocks have held up quite well in recent months, despite overall weakness in the oil price. A much better buying opportunity could well emerge next year however if a risk-off sell down in equity markets occurs, while at the same time we cannot rule out further crude price weakness given rising recessionary risks for CY23.

Crude oil

US employers added 263K jobs to payrolls in November, topping market forecasts of 200K, and following an upwardly revised 284K additions for October. It was the lowest job gain since April 2021, as the jobs market is normalizing after the pandemic turmoil. Nevertheless, the pace of additions was well above the typical pre-pandemic range of about 150K-200K jobs added per month. There were notable job gains in leisure and hospitality (88K); health care (45K); and government (42K). Employment declined in retail trade (-30K); and in transportation and warehousing (-15K).

Non-farm payrolls report

The unemployment rate was unchanged at 3.7% in November, matching market expectations and not far from September’s 29-month low of 3.5%. The unemployment rate has hovered in a narrow range of 3.5%-3.7% since March, indicating a tight jobs market.

Unemployment rate

Finally, average hourly earnings increased 0.6% monthly in November, following an upwardly revised 0.5% increase in October and coming in at double expectations for a 0.3% monthly rise. On an annual basis, average hourly earnings have increased by 5.1%, above the 4.9% pace in October and well above market expectations for a 4.6% rise and heightening worries about a wage price spiral.

Average hourly earnings change (YoY)

There was little in the above batch of data that would convince the Fed to slow down policy tightening much, although markets are still expecting a 50-basis point hike this month, rather than another 75-basis point hike. The key now is where will the terminal rate end up? I still think the terminal rate settles between 4.5% and 4.75% next February given the growing cognisance of the Fed about existing tightening – which is the steepest and fastest on record given the low starting point. The Fed now needs to stand back and assess the broader transmission impact on the US economy or risk “overtightening the screws” and delivering into the bond markets expectation of a recession next year.

Sectors were mixed on Friday, with materials (1.1%), industrials (0.6%) and consumer staples (0.4%) leading the way higher, while Energy (-0.6%), tech (-0.55%) and utilities (-0.5%) were the biggest losers.

Mega-caps were a slight drag overall, with the Vanguard Mega Cap Growth index 0.2% lower. A 2.5% advance for Meta capped losses, while Microsoft edged up 0.1%, as did Tesla and Amazon shed 1.4%, Alphabet was 0.55% lower and Apple dipped 0.3%.

The Wall Street Journal reported that Apple is prompting suppliers to plan to shift production more actively outside China, to reduce reliance there. India and Vietnam are atop the list for alternatives. In the past few weeks, tensions at Foxconn’s (Apple’s biggest assembler) boiled over, disrupting iPhone Pro production at the Zhengzhou facility, the world’s largest iPhone assembly plant. This could crimp production by 10-20% according to a range of estimates.

The move to reduce reliance is a welcome one and therefore I suspect the WSJ article is on point. The reality is that to meaningfully reduce reliance on China ‘and reshoring production capacity elsewhere’ will be a multi-year process. Sentiment towards Apple is unlikely to improve anytime soon. Still Apple’s customer base is more resilient than average, and demand should mostly remain intact, despite some supply shipments moving to the March quarter.

Apple remains technically well supported at the $140 level however, recent price action has been bearish. The stock likely faces a key test of the $140 support level in coming months with a downside break the most plausible scenario, as supply and production issues collide with what is an expensive valuation

Enphase Energy (7%) topped the S&P 500 gainers table after the solar energy tech firm announced the launch of microinverter sales in France and the Netherlands, the first expansion into international markets for the product since launch in North America late last year. This dragged Solaredge Technologies some 4.4% higher on the read-across and as the Commerce Department released a preliminary report saying Chinese solar manufacturers have been skirting tariffs.

Cloud security firm Zscaler shares slid 10.7% despite a strong quarterly earnings report and guidance. The company beat on the top and bottom lines. Although billings growth was still strong, there was a slowing of momentum, and the broader cloud-related space continues to be de-rated from lofty valuation levels. Asana, a work management platform, fell 10.5% after reporting a narrower loss and providing softer than hoped guidance.

Marvell Technology, one of the leading memory chip companies, dipped 1.5% after missing with its quarterly numbers and issuing underwhelming 4Q guidance. Tech firm PagerDuty on the other hand advanced 5% after a small profit topped expectations for a quarterly loss. The firm beat on the top line as well. Biotech Horizon Therapeutics advanced 3.9% as Sanofi reportedly said that if it decides to make a firm bid, it would be an all-cash offer. Earlier last week, Horizon said the company was in preliminary discussions with several pharma companies for potential takeover offers. Ulta Beauty (-0.2%) closed little changed, despite a beat-and-raise quarter.

DoorDash skidded 3.4% following a downgrade from RBC Capital Markets to sector perform with the brokerage reportedly citing intensifying competition from Uber as part of the rationale. Uber advanced 1.5%.

Gold prices edged lower, but exposures were mixed. Hecla Mining, ETFMG Prime Junior Silvers Miners ETF and VanEck Junior Gold Miners, while Coeur Mining, Harmony Gold and some others were lower. The Sprott Physical Uranium Trust (-0.5%) as did the Invesco DB Agriculture Fund (-0.3%). The energy service giants Halliburton and Schlumberger advanced 2.6% and 2%, despite the broader energy sector being under pressure. As I have noted before, these companies should enjoy strong order books for years to come.

Elsewhere, Peloton shares surged 13%, seemingly as a few more short sellers decided to cover, with the shares doubling from lows endured earlier in the year, although still some sharply lower over the past year. US-listed China shares continued to advance on Friday on reopening hopes, with JD.com, NetEase, Tencent Music and others staging strong advances. Wynn Resorts (1.3%) logged an advance as its subsidiary (Wynn Macau) gained in Hong Kong trading.

One of the market’s pandemic darlings, Peloton now looks to be bottoming out. The company has been pressured by falling demand in the wake of the pandemic and reopening, but after significant restructuring, the company seems to be on the mend operationally. Better times likely lay ahead for the stock price, which is inflecting off what has been lengthy period of base building

Turning to Australia, the ASX200 was down 0.72% to 7301. The best performing sectors were Healthcare (+1.09%) and Communication Services (+0.82%). The worst performing sectors were Real Estate (-2.63%) and Energy (-2.45%). The SPI futures this morning point to a 0.26% increase on the open.

Some of the major banks have released their expectations for tomorrow’s announcement from the RBA and the rate tightening path for 2023.

HSBC believes the RBA will lift rates by 25 bps on Tuesday, despite a tight labour market and elevated inflation. HSBC also forecasts a pause in monetary policy after December as the RBA assesses the lagged impact of rate hikes on the economy. This is fairly bullish considering inflation has yet to really peak in Australia and given the RBA’s cash rate is now well below that of the US and NZ.

CBA’s economists are forecasting a 25 bps hike in December 2022, bringing the cash rate to 3.1%, and also then a pause. However, CBA still believes it possible the RBA could choose to hike by a further 25 bps in February 2023 if a tight labour market persists. The bank argues that the RBA will opt to keep rates steady because of a dangerously leveraged housing market. The labour market could also still be stubbornly tight by then, which might just defy economist forecasts.

Meanwhile, Westpac economists expects the RBA to raise by another 100 bps between now and mid-2023, which implies four additional 25 bps hikes in December 2022, February, March and May 2023. Westpac also forecasted Australia’s GDP to grow at 0.8% in the September quarter, which pushes annual growth to 6.4%. WBC expects growth to be robust in the September quarter but sees a sharp slowdown in 2023 due to the full effects of inflation and rising interest rates hitting the economy. This is already evident in retail sales declining for the first time in many months. I don’t this scenario playing out either given the still massive leverage in the housing market and the fact that we are yet to see the economic impact of $500 billion in fixed rate mortgages repricing. Many homeowners rolling their mortgages will not be able to maintain servicing.

ANZ is similar to WBC in their outlook seeing 25 bps rate hikes in December 2022, February, March and May 2023, which would see a peak of 3.85% and expects the RBA to keep rates on hold until November 2024, whereby the first cuts would start.

NAB forecasts 25 bps in December 2022, February and March 2023, then a subsequent pause and hold by the RBA till 2024. This scenario seems more plausible to me given the transmission risks through to the housing market.

As the RBA’s decision will be highly data dependent, and they will stick to the script of 25 bps in December 2022, with a few more hikes to follow in 2023. Much will come down to the housing market and how it navigates the tightening cycle but also just how effective government intervention will be on energy prices. Inflation could also come down faster than expected (as I am anticipating in the US), which could provide the RBA with more flexibility.

Moving on, soaring iron ore, coal and natural gas prices are now estimated to add $58 billion to tax revenues over the next 4 years and place the federal budget bottom line temporarily in balance. Thermal coal prices alone will add $5 billion to the budget in 2022-23 and $15 billion in 2023-24 according to veteran budget forecaster Chris Richardson. Interestingly, the October budget forecasts thermal coal to fall to US$60 per tonne by March 2023, while coal futures are trading way above this level at US$360-390s.

Barchart – ICE Newcastle Coal

While this is all great for the budget getting back into balance, structural spending pressures on social services and defence should see the bottom line head back to negative territory for the foreseeable future.

On to stocks, Solomon Lew’s Premier Investments reported a 23.6% increase in global sales in the first 17 weeks of FY23, compared to pre-pandemic levels in 2020 – which is a solid outcome. However, the retailer noted that the last 5 weeks to date sales being flat compared with a year ago, when stores reopened and boomed after a 4-month Delta lockdown. There is a question mark over the busy and important Xmas trading period, which is make or break for many of Australia’s retailers. We will soon know after Xmas and the busy sales period just what the impact is going to be of the RBA’s rate hikes and their impact on the real economy and discretionary consumer spending.

On outlook, Premier management said the company was well positioned to capture the current momentum leading into Christmas, Boxing Day and “Back to School” sales. They were also confident that despite higher interest rates, a tight labour market and an expectation of higher wages would not see spending fade away. As analysts liked to hear, the management team confidently noted they were well-placed to materially beat consensus expectations for 1H23.

In my view, cyclical retailers have always been uncertain but given Premier’s strong performance in FY23 despite sharp rate hikes, it appears that their strategy has helped them navigate tough trading conditions.

Brands like Smiggle should continue to perform strongly, given kids need school equipment like bags and stationery, which are items that will usually not break the bank, thus should have relatively little setback even if Australia enters a deep recession.

I think it’s best to avoid the whole retail sector in a downturn, but there will always be some retailers who demonstrate growth regardless. Premier’s shares were muted on Friday as the market was likely forward-looking to next calendar year’s performance – this is usually a good sign that the market was not greedy and expecting more. We do not hold shares.

Premier remains well down form the highs above $32 and below near-term resistance at $26 which does not look like being breached on the topside for some time. The longer term technical setup remains favourable however with the shares holding in comfortably above the primary uptrend

On Friday, it was reported that Andrew Forrest has bid for Chalice shares that were owned by former chairman Tim Goyder (a special cross trade will likely happen). The total holding represents 8.8% of Chalice, which appears to be a starter position for Mr Forrest to purchase more – the average price was $5.71, with a total shareholding of $189 million.

While Mr Forrest did not provide commentary, it might be worth thinking about why. In my view, there will be consolidation in the resources sector as Australia’s energy transition plays out, especially for producers with mature assets in well-placed geographies. As a result, this could result in a Chalice takeover in the future. Furthermore, shares have fallen close to 40% from highs and have consolidated technically, which could also be a precursor to a takeover bid. We hold Chalice Mining shares in the Managed Accounts.

Chalice has broken above near-term resistance which is encouraging technically and points to further topside extension. A pull back and retest of the $5.50 level is probable in the months ahead, but the shares look to have established a meaningful inflection

Turning to Asia, the CSI300 index tracking large caps listed in Shanghai and Shenzhen declined 0.61% while the Hong Kong benchmark dipped 0.33%, retreating slightly from a 3-month high with traders taking a breather after some strong gains earlier in the week as they recalibrated thinking about how quickly a mainland China reopening could take and that even with the recent support outlined for the property sector, the problems are large.

Reuters cited rating agency Moody’s as writing, “The outlook on the (property) sector remains negative because of sluggish demand, and while the government’s new policies could ease funding constraints, they will take time to have an effect.” While Nomura cautioned “the path to ‘living with Covid’ may still be slow, costly and bumpy”.

President Xi Jinping met with Charles Michel, the European Council President on Thursday in Beijing and reportedly implied the spread of the less severe Omicron strain might be helpful in easing zero-Covid policy. Media cited officials speaking on condition of anonymity as Xi Jinping saying to Charles Michel that demonstrators were “mainly students or teenagers in university.”

The Hang Seng advanced 6.3% for the week and as I noted last Thursday had a tremendous November on the prospects for an off-ramp from the tortuous almost 3-years of draconian zero-Covid policy. The CSI 300 did not have as strong a week as the Hang Seng but still rose 2.5% over the week.

There have been more supportive developments over the past few days for both the key headwinds for the Chinese economy. Cities in China are taking an individual approach to easing restrictions, but they are occurring, whether it is loosening restrictions for districts in lockdown, allowing some low-risk people to isolate at home, ceasing mass-testing and notably, a softer tone from Beijing about the dangers of Covid. At the same time, officials are talking up a push for vaccination of the elderly and vulnerable.

As Citi noted, “the government is clearly moving actively towards reopening instead of doubling down pandemic control measures”. Beijing removed Covid-19 testing booths and Shenzhen will no longer require test results for travel, both major quality of life improvements.

There were no major economic releases on Friday with the private Caixin survey services PMI due today and inflation data due out later in the week, although unlike most countries, inflation hasn’t been running hot in China and therefore the data is unlikely to be as influential to sentiment as it has been in 2022 for the Western markets.

In Hong Kong trading, Chinese real estate developers led the decline, along with financials. Traders were taking some profits after developers jumped in November as Beijing lifted support to increase liquidity in the industry and stave off more defaults. Longfor Group shed 4.3% and and Country Garden slid 4%. Meanwhile, financials like CITIC (-4%) and Industrial & Commercial Bank of China (-2.3%) were also in the red at the close.

On the other hand, the decline in the index was limited thanks to solid gains for some tech stocks and consumer exposures as traders tweak reopening bets. November was marked by some beaten-up stocks soaring on speculation, such as the developers. Hotpot chain Haidilao International was an example, although its strong performance continued on Friday, up 7.1%.

Haidilao has broken above meaningful overhead resistance after establishing a new base above support for much of the year. An inflection now looks to be in

The restaurants are known for their communal dining experience and are generally boisterous places where a group of friends may like to unwind after a tough day at work, sharing a bit spicy hotpot and a few beers or a bottle of Baijiu (the classic Chinese liquor). Zero-Covid policy devastated that business and the stock price and traders have piled in off late, lifting the stock by more than 40% over the past month.

The recent gains haven’t been quite as dramatic for brewer Budweiser APAC and KFC/Pizza Hut operator Yum China but neither were they hit quite as hard given more resilient businesses, they were up 1.3% and 2.4% respectively on Friday.

The Macau casino operators are another sector that has been decimated by the pandemic. Last week the sector benefitted from reopening optimism and the extension of 10-year provisional concessions to keep operating in Macau, the only legal gambling hub in China. On Friday, Wynn Macau was up another 4.3%, MGM added 4% and Sands China missed out by dipping 0.5%.

Tech stocks had a good day, led by Alibaba Health Information (9.7%). Food delivery platform Meituan rose 3%, Alibaba Group was up 2.4% and Tencent added 0.5%, with the odd one in the group Baidu, slipping 0.7%.

Elsewhere, China Oilfield Services was up 0.8%, while local bourse operator Hong Kong Exchanges and Clearing dipped 0.6% and gold miner Zhaojin was 1.1% lower.

In Japan, the Nikkei and Topix declined 1.59% and 1.64% on Friday. The Nikkei retreated to its lowest level in three weeks. While there were no major local economic releases, the recent yen strength against the weakening dollar hit exporters, particularly the automotive ecosystem, a very important group in Japan. Investors were also cautious ahead of the monthly US non-farm payrolls report due out later in the day, which can influence the Fed policy on interest rates.

Japan had another cracking result at the World Cup, beating Spain (2-1) and that boosted shares of online broadcaster Cyber Agent (4%) and British-style pub chain Hub Co (7%).

On the other hand, as noted earlier, a stronger yen dragged on automakers, with Mitsubishi Motors the worst performer, skidding 5.9%, while Nissan was down 3% and index gorilla Toyota shed 1.4%. Uniqlo owner Fast Retailing was the biggest drag on the Nikkei, falling 1.7%, despite the company having a strong presence in mainland China. Again, the stronger yen was likely the headwind here.

Industrials were mostly lower. Component maker THK Co (-2.6%), Apple supplier Alps Alpine (-1.8%), touch screen sensor firm Nissha Co (-1.1%), robotics expert Yaskawa Electric (-0.9%) and air-conditioning giant Daikin Industries (-1.4%) all closed in the red.

Financials were also generally lower, although Dai-Ichi Life was an exception on Friday, inching 0.2% higher. Megabanks Sumitomo Mitsui and Mizuho Financial were down less than 1%, while Mitsubishi UFJ, Resona Holdings, Nomura, Chiba Bank, Concordia and Fukuoka Financial fell more than 1% and Mebuki Financial slipped 2.6%.

The video games cluster of Sony (-1.3%), Nintendo (-1.4%) and Square Enix (-0.8%) was underwater at the close. Elsewhere, oil & gas producer Inpex was shed 2.3% and food ingredients firm Ajinomoto edged up 0.3% on its defensive appeal. As I noted last Friday, the shares have been strong gainers this year, given a dominant position in its niche in Japan, where its products are found in most households and restaurants, along with overseas growth opportunities and progress to mitigate cost inflation.

The FTSE 100 was a tad lower (-0.03%) and FTSE 250 declined 0.24% as traders digested higher than expected payrolls and wage data from across the pond in the United States. Sterling strengthened against both the greenback and the euro. It was a quiet day for corporate news.

On home shores, the latest BDO high street sales survey showed total like-for-like sales increased 4.3% in the week ended November 27, as shoppers took advantage of Black Friday sales. Still, that was a far cry from the roughly 39% surge a year ago, which also included Black Friday, highlighting caution for UK shoppers amid the cost-of-living squeeze.

Another set of data – the BRC-SensormaticIQ footfall monitor – showed for the four weeks ended November 26, total UK footfall rose 3.7% year-on-year. Within that, high streets footfall increased 8%, in shopping centres it was up 7% and fell 4% in retail parks. Compared to pre-pandemic levels, however, footfall fell 13.3%, some 1.5 percentage points below October, and worse than the three-month average decline of 11.5%.

“Footfall took another stumble as the cost-of-living crisis put off some consumers,” said Helen Dickinson, BRC chief executive. “Others opted to stay home due to the scattering of rail strikes or chose the World Cup over shopping visits. Rising inflation and low consumer confidence continue to dampen spending expectations in the run up to Christmas.”

On the corporate side, budget airline Wizz Air reported passenger numbers flew 70% higher year-on-year in November to 3.68 million. The shares ascended 2.7%. The travel and leisure group had a decent day overall. British Airways owner IAG (0.9%) and budget airline easyJet (1%) ascended on the read-across from Wizz but cruise ship operator Carnival sank 4% to be an exception. Travel location café and restaurant operator SSP Group had a solid day, up 4.05%, while staycation beneficiary PPHE Hotels added 0.8%.

SSP Group shares advanced ahead of their preliminary full-year results due early this week. An earlier reported pre-close trading update from SSP Group reported a strong fourth quarter, with revenues expected to be at circa 91% of 2019 levels, driven by a continued recovery of passenger numbers even amid some travel chaos over the summer. This includes the benefit from net contract gains and price increases compared to the same period in 2019.

The recovery is being led by domestic and leisure travel across both the Air and Rail sectors, with business and commuter travel also recovering. In the quarter there was a recovery in trading across all our regions, with Continental Europe (circa 95%) and North America (circa 95%) the closest to pre-pandemic levels. The company did note passenger numbers remain very low in China and Hong Kong. A recovery here is something for SSP Group to look forward to in 2023.

SSP Group are close to staging a topside inflection and breaking overhead resistance after an extensive period of ranging and consolidating above key support

Associated British Foods, for which the Primark retail chain is also a core business, gained 5% to top the large cap gainers table as Goldman Sachs blessed the stock with an upgrade to ‘neutral’ from ‘sell’ as the price target was given a big boost from 1460p to 1900p a share. Back in September AB Foods warned that rising costs and slowing demand would hit profits, sending the shares to a 10-year low, bringing down the hurdle for outperformance.

Morgan Stanley was even more positive than Goldman with an ‘overweight’ rating, despite the same 1900p target price. The shares closed at 1,667.5p. Morgan Stanley noted the cost pressures in the food business but believes AB Foods is better placed than many to weather the storm.

Buffering the FTSE100 from steeper losses on Friday were advances for banking stocks as US Treasury yields shifted higher in early trading. NatWest added 1.8% and Lloyds advanced 1.1%.

Packaging firm DS Smith was up 1.3% and peer Mondi added 0.9%. The research team recently noted on DS Smith that while cost inflation is sweeping across the globe, particularly in the UK and Europe, DS Smith continues to be adept in managing this stress. The company is pushing through price increases without too much pushback on volumes to date. Sky-high energy prices are being mitigated through energy efficiency initiatives in part, but largely through a long-term hedging programme. In the trading update from September, DS Smith noted that more than 90% of natural gas costs were hedged for FY23 and circa 80% for FY24.

In the commodities complex miners BHP (0.2%), Rio Tinto (-0.9%) and Glencore (0.3%) were mixed. Energy majors BP (-1.7%) and Shell (-0.7%) declined, as did small cap waste-to-energy firm Powerhouse Energy (-2.5%). Precious metals miner Fresnillo dipped 0.8%.

Elsewhere, Domino’s Pizza warmed up 1.8%, while BT Group eked out a marginal 0.1% advance. The online classified leaders Auto Trader (-0.3%) and Rightmove (0.2%) were mixed. Rolls-Royce (3.8%), Pets at Home (2.4%), Greggs (2.05%) and ITV Plc (2%) advanced. We hold BT Group, PPHE, Fresnillo, Carnival, Powerhouse, Rightmove, Auto Trader, Domino’s, Shell, SSP Group, Rio Tinto, and BHP. The research team covers those along with BP, IAG, easyJet, Glencore, easyJet, DS Smith, Rolls-Royce, Pets at Home, ITV and Greggs.

On the continent, producer price inflation in the Eurozone slowed sharply to 30.8% year-on-year in October, down from September’s reading of 41.9% and the record high of 43.4% back in August. The October figure came in slightly below market expectations of 31.5% and remains very elevated from a historical perspective amid the energy crisis. Excluding energy, producer prices would have increased 14.0% year-on-year in October, decelerating from 14.5% in September.

Eurozone factory gate inflation (YoY)

European stocks generally dipped as the US jobs report and wage increases came in strong, dampening hopes somewhat for a dovish Fed pivot. A modest advance in Germany’s benchmark index was an exception as Europe’s largest economy still managed to record a trade surplus, albeit a little smaller than a year ago. Exports dipped by 0.6% but imports fell 3.7%, with the trade surplus standing at €5.3 billion, down from €12.5 billion a year earlier.

At the close the pan-European Stoxx 50 was down 0.17%, Germany’s DAX added 0.27% and France’s CAC-40 dipped 0.17%. Italy’s FTSE MIB declined 0.26% and Spain’s IBEX 35 was in the red to the tune of 0.30%.

Carpe Diem!

Angus

Disclosure: Interests associated with Fat Prophets hold shares in Apple, Alphabet, Uber, Wynn Resorts, Peloton, Halliburton, Schlumberger, Hecla Mining, Coeur Mining, Harmony Gold, ETFMG Prime Junior Silver Miners, VanEck Junior Gold Miners ETF, Sprott Physical Uranium Trust, Invesco DB Agriculture Fund, Alibaba, Baidu, Tencent Holdings, Hong Kong Exchange and Clearing, Yum China, Budweiser APAC, China Oilfield Services, Zhaojin Mining, MGM China, Sands China, Wynn Macau, Sony, Nintendo, Square Enix, Daikin, THK Co, Nissha Co, Yaskawa Electric, Sumitomo Mitsui, Mitsubishi UFJ, Mizuho Financial, Resona Holdings, Mebuki Financial, Nomura, Concordia, Chiba Bank, Inpex, BT Group, PPHE Hotels, Fresnillo, Carnival, Powerhouse Energy, Rightmove, Auto Trader, Domino’s Pizza, Shell, SSP Group, Rio Tinto, BHP and Chalice Mining.