The next super cycle

The next super cycle

The next super cycle

Key topics discussed today include:

Not over till it’s over – A noted hawk, James Bullard thinks markets are underestimating the chances of higher interest rates. We are in for a bumpy Christmas

Friedmann Equation – Protests sending a message to Beijing that enough is enough on covid restrictions, while Chinese equities continue its decline. Could we see a possible full reopening soon?

Equities still have room to fall – Goldman Sachs’ Peter Oppenheimer argues markets will only reach a bottom when interest rates come down, and we are yet to get there

Once it stops hiking, it’s easing – Morgan Stanley’s Andrew Sheets sees US Fed’s final rate hike in January but equities still under pressure from dismal earnings into 2023

Too much oil? – OPEC considering cutting supply due to faltering global demand, while Russian output stands to slump in early 2023. What sort of price action can we expect from the WTI?

India’s economic ascendance – The rise in the nation’s energy consumption opens a new segment to boost investment growth; Could this set the scene for the next commodities super cycle?

Just around the corner – More pain is coming into the Australian housing market as the full effects of interest rate rises crystallises

Below asking price – UK housing market demand falls 44% while homeowners were generally forced to accept prices below asking

Notable stocks and indices mentioned include the S&P500 Index, WTI Crude Oil, The Nasdaq Golden Dragon Index, Pinduoduo, Apple, Telstra, Bank of Queensland, Wynn Macau, Inpex, and BT

Good morning,

Wall Street declined on Monday, as protests in major Chinese cities against covid lockdowns and restriction weighed on commodities and the global growth outlook for next year. The concern is that the protests will gather momentum, disrupt supply chains, dampen demand for commodities and lower global growth in the new year. The S&P 500 energy index and the materials index both slid 2.74% and 2.2% respectively, as the biggest sector decliners. The Dow Jones was down 1.45%, the S&P 500 lower by 1.54% to 3963 and the Nasdaq Composite fell 1.58% as technology and growth stocks fared better.

Oil fell sharply earlier in the session but lifted into the green late afternoon in a strong reversal, after OPEC insinuated production cuts. WTI crude oil lifted 0.45% to $76.62. US bond yields edged lower with the 10 yr and 30 yr falling between 1 and 2 bps. Volatility rose 8% with the VIX rising back above 22. The US dollar index rose 0.5% to 106.5. Base and precious metals were all softer.

Also weighing on stocks was more Fedspeak which came ahead of Fed Chair Powells scheduled speech due on Wednesday, which will provide the next round of impetus with markets along with key economic data including jobs and PCE inflation on Thursday and Friday. Fed Bank of St. Louis President James Bullard (a noted hawk) said “markets may be underestimating the chances of higher rates” while New York counterpart John Williams noted policymakers “have more work to do to curb inflation.” The comments pushed up the US dollar rose and bond yields.

While Fed Chair Powell will no doubt also push back and emphasize a “stronger-for-longer” labour market and tight monetary policy, the bond market is seeing sharply slowing growth and inflation next year with a steep yield curve inversion. The big question is whether the rebound rally can sustain itself into the December?

Technically, the S&P 500 is pushing up against the primary bear market trendline. To break through on the upside and sustain the rally, the SPX is going to require the “right narrative” from Jerome Powell who needs to adhere to the script that there is an end in sight to the tightening path, on Wednesday. Markets will also need to see softer PCE inflation and labour market prints on Thursday and Friday. Resistance from the bear market trendline is formidable and so the ‘cards need to fall’ in the right way for the rebound rally to be sustained.

Earnings are also going to come into focus within a matter of weeks. The xmas rally will soon face further significant headwinds in four to eight weeks, as the market changes gear and focus turns from inflation and rates, to what the outlook for the corporate sector earnings look like in CY23.

S&P 500

Meanwhile, the latest wave of covid in China is likely to accelerate the path of reopening next year, but the protests have sent a message to Beijing that ‘enough is enough’ on the lockdowns and restrictions. President Xi has pushed the population to the limit on this front and will have to now prepare China for a full reopening possibly late in the 1st quarter of next year.

The uncertainty over the covid surge and accompanying restrictions could however see the CSI300 retest the October lows in the weeks ahead. It is also likely the rally in commodities, energy and precious metals could be checked as economic activity and demand remains in check. Goldman Sachs warned this week of a ‘messy exit’ from Covid’ with civil unrest adding another layer of uncertainty over the economy.

Goldman Sachs chief equities strategist Peter Oppenheimer warned that the market is still a long way from seeing stocks hit a bottom or interest rates coming down. “Mr Oppenheimer said in a Monday interview on Bloomberg “we don’t typically get markets reaching a trough until interest rates start to come down, and we’re still a little way away from that,” and was dismissive of recent gains spurred by China’s reopening, falling gas prices, and cooling inflation.

“Equities still have room to fall, with the S&P 500 still expensive trading on a price-to-earnings multiple of 17x, which is a sign that stocks are still considerably overvalued. Despite the recent rally, US earnings growth could clock in at close to zero next year, with a more severe slowdown in European earnings. I don’t believe a decline would be that severe, with bank and corporate balance sheets still strong, and the US will likely avoid a hard landing.”

“However, I think the market is going to be exposed on margin to more difficult news to come through, particularly on growth in the coming months. And we don’t think we’ve hit yet the sort of conditions that we would typically see in a genuine trough in the bear market, that helps form the case for a sustained rebound.”

Meanwhile Morgan Stanley’s cross asset strategist Andrew Sheets said that the “Federal Reserve’s last rate hike could come as soon as January, but stocks will still be under pressure from dismal earnings into 2023. We are in the camp that the Fed will be early to pause. We think the last Fed hike is in January. Inflation is showing clear signs of coming down, potentially causing the Fed to pause its monetary tightening regime earlier than expected” Mr Sheets said in an interview on Bloomberg last week.

“After its last rate hike in January, the Fed will likely hold its policy rate and continue monitoring the economy to see the full effect of its tightening so far. There is still a lot of uncertainty on inflation’s trajectory next year. But central bankers risk undoing the tightening they’ve done so far by pausing rate hikes. Can the Fed really pause without reversing the progress that it’s made in tightening financial conditions? Almost by definition, once it stops hiking, it’s easing. And does that work against everything the Fed is trying to achieve? How does it message that, I think is a really big debate.”

Moving onto oil, OPEC is now expected to consider deeper supply curbs when the cartel meets this weekend against the backdrop of a faltering global demand. Saudi Arabia drew the ire of President Joe Biden when they supported a production cut of 2m barrels last month, prompting a further release of oil reserves from the Strategic Reserve. Delegates from the group, who until this week had predicted they would pause to assess the impact of the cuts, now say additional reductions could be an option. Saudi Energy Minister Prince Abdulaziz bin Salman said OPEC+ was “ready to intervene with further supply reductions if it was required to balance supply and demand.”

Meanwhile, Russian output stands to slump 15% early next year, as price caps begin to bite on supply. Inventories are also on the low side. OPEC has regained pricing power with the decline in the US shale oil output and the chronic underinvestment within the sector over the past ten years. The fall in WTI crude prices into the $70s could well elicit a response from OPEC and keep prices within a range until China reopens and global demand returns to pre pandemic levels.

The forward curves for Brent and WTI which are the two main international benchmarks, have developed a discount for near-term contracts known as a contango in futures markets. The price pattern typically signals oversupply and encourages refiners to hoard unwanted barrels. OPEC views the contango negatively and this could prompt a supply cut as early as this weekend. WTI oil is precariously perched on key support at the $77 level. If a downward break ensues below this level during the week, then the commensurate risks will grow of an OPEC production cut this week

I have written a lot about China this year and the prospects for lower growth over the coming year. The growth slowdown in China is however also a structural story as the economy transitions away from a property and infrastructure investment led expansion to one more dependent on domestic spending. While covid lockdowns have impacted China and expedited this trend, looking ahead China GDP will no longer be growing at prints of 10% to 12% but 4s and 5s, and possibly even at much lower levels over the longer term.

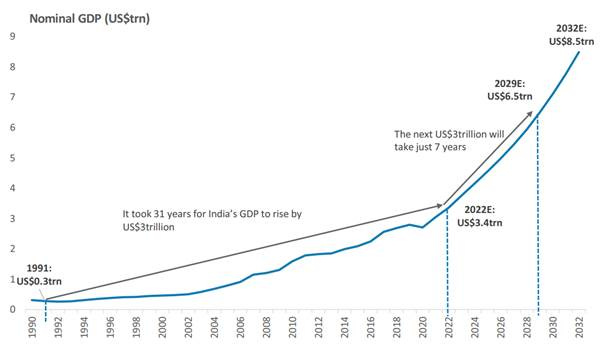

One global growth engine that is emerging that will propel one economy to becoming the third largest in coming years is India. The world’s largest democracy, India is growing at a fast pace reminiscent of where China was 15 to 20 years ago. And India is set to pick up where China leaves off in the decade ahead, which will provide a powerful tailwind for the next commodities super cycle.

India is already the fastest-growing economy in the world, having 5.5% average GDP growth over the past decade, and is poised to become one of the top economic powerhouses to the world, as corporate tax cuts, investment incentives and infrastructure spending drive capital investments in manufacturing. Digitalisation and energy transition is also setting the scene for unprecedented economic growth.

Morgan Stanley thinks India’s GDP could more than double from the US$3.5 trillion today to surpass $7.5 trillion by 2031. Its share of global exports could also double over that period, while their equity markets could deliver 11% annual growth for investors in the next decade.

Although India will need to tap fossil fuels to meet its growing energy needs, an estimated two-thirds of India’s new energy consumption will be supplied by renewables like biogas and ethanol, hydrogen, wind, solar and hydroelectric power. This could reduce the nation’s reliance on imported energy and improve living conditions in a country that is home to 14 of 20 most polluted cities on the globe. This wave is also creating new demand for electric vehicles, bikes and green hydrogen-powered trucks and buses.

The rise in India’s energy consumption alongside the energy transition opens up a new segment to boost investment growth and I can see this rise in capital investment unleash a second “super virtuous cycle” of investment. However, investing in India is a long-term theme, with a share of risks including lack of skilled labour, energy shortages and adverse geopolitical developments, but these were all issues faced by China two decades ago.

The medium to longer outlook for commodities therefore is likely to remain intact, as India grows to become the world’s third largest economy. This year the global economy was hit by a commodities “super-squeeze” rather than a “super-cycle,” as underinvestment in traditional fossil fuel sources conspired to drive prices higher.

Part of the “squeeze” was caused by geopolitical issues and the Russia-Ukraine war, however the “energy transition” itself has limited large-scale investment in oil, gas and coal capacity. The OECD believes the current global energy price crisis to be as severe as the 1970s. Spending among OECD nations on electricity, natural gas, oil and coal has soared to almost 18% of collective global GDP in 2022, up from 10% in 2021.

However, unlike the China-sparked super-cycle of the late-2000s, the latest price shock has not resulted in any material increase in investment, which could keep energy prices elevated in the years ahead. While oil remains under near-term pressure and Wall Street has likely yet to complete a bear market bottom, energy and commodities should be on investor shopping lists over the coming months when stocks find an important low.

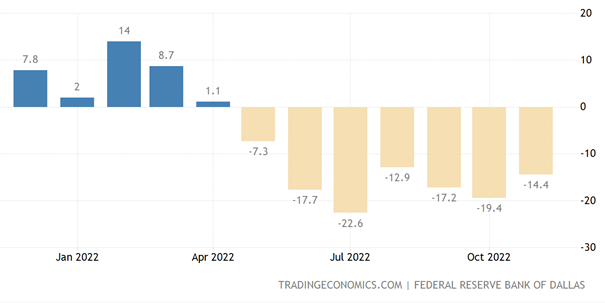

On a quiet day for local data, the Federal Reserve Bank of Dallas’ general business activity index for manufacturing in Texas increased to -14.4 in November from -19.4 in October. The prices paid for raw materials fell sharply, leading to lower inflation in selling prices. The production index fell to just 0.8 points from 6 in the prior month, indicating a deceleration in output growth. New orders were negative for a sixth straight month. Still, firms were a little more optimistic about the outlook.

Dallas Fed Manufacturing index

While Asian markets were under pressure due to Chinese protests, US investors had a different spin on the outlook Monday afternoon, supporting US-listed Chinese shares. The Nasdaq Golden Dragon Index has fallen sharply for close to 75% in the past two years in what has been a ferocious bear market. However downward price action appears to be dissipating and the Index looks to have formed an important bottom. The fact that the index managed to rise 3% on Monday points to the market looking through the latest covid wave and protests to an earlier reopening in China.

Meanwhile, many Chinese listed companies are exceeding earnings estimates by a wide margin which might just mean an important inflection is now in. A breakout in the index looks to be nearing which would confirm an important inflection is in and put an end to one of the longest bear markets for Chinese equities.

Nasdaq Golden Dragon Index

A solid third quarter report from Chinese e-commerce player Pinduoduo sent those shares surging +12%. Revenue surged 65% year-on-year to 35.5 billion yuan ($4.99 billion), well above the consensus of 30.9 billion yuan. Consumer electronics, beauty products and agri products fared well according to management commentary.

Pinduoduo, first competed in smaller Chinese cities but has since taken on the likes of Alibaba and JD.com in top-tier cities. Recently the company has gambled by launching an international platform (Temu) to sell made-in-China products, largely affordable ones to US consumers. The platform has emerged as a competitor to Shein, which has a similar business model targeting consumers in the West with affordable Chinese products.

Non-GAAP operating profit came in at an impressive 12.3 billion ($1,73 billion), soaring increase 277% year-on-year. Net income was 10.59 billion yuan ($1.49 billion), an increase of 546%. Adjusted EPS of $1.21 per share was almost double the $0.65 consensus estimate.

Pinduoduo broke out above resistance at $70 on Monday, which likely confirms the stock has bottomed and an inflection is now in

While many US-listed shares of Chinese stocks were on the rise, including audio streamer and publisher Tencent Music, companies with substantial exposure were also getting a boost on hopes protests can push through a quicker end to zero Covid policy. On the other hand, there is a risk the protests could push through a more authoritarian regime from Xi Jinping as he just recently stacked his cabinet with hardliner supporters. It’s hard to know where the chips will fall currently. Still, the Invesco Golden Dragon ETF was up strongly late afternoon even as the broader market was lower.

Casino owners Wynn Resorts, Las Vegas Sands and MGM Resorts advanced as they benefited from their Macau subsidiaries being granted new provisional licenses to continue operating in Macau for an additional 10 years beginning from January. Now, the businesses just need to look forward to a further easing of restrictions on testing and travel from mainland China.

Apple on the other hand was under pressure on the likelihood that the tech titan will face a substantial iPhone Pro production shortfall due to Covid-related unrest at Foxconn’s massive assembly plant in Zhengzhou, China. Indeed, Bloomberg cited a person familiar with matter saying the shortfall could be close to 6 million iPhone Pro units. That would be a blow given the higher margins on the Pro units, which are in high demand. Bloomberg reported that Apple and Foxconn expect to be able to bridge the shortfall in 2023, however, the situation is fluid. Earlier, Bloomberg had already reported Apple has lowered its total production target for iPhones to approximately 87 million units from an earlier target of 90 million units.

Apple is converging within a triangle pattern with the stock weakening towards the lower end of the range. This raises the prospects of a downside break in coming months and a fall back towards the $120 level

Mega-caps were a drag overall with Alphabet, Microsoft and Meta also lower, while Amazon and Tesla advanced. Facebook parent Meta was fined the equivalent of $276 million by a European regulator for not better safeguarding user data. The fine was barely a slap on the wrist for a company of Meta’s size.

Disney shares were in the red as the company’s latest animated release, Strange World flopped at the box office. The sci-fi feature from Disney Animation Studios took in just $18.6 million over its first five days at the North American box office. The international numbers weren’t any better, generating just $9.2 million according to reporting from industry site, Box Office Mojo. Raya and the Last Dragon only took in $8.5 million from its North American opening at the box office but was released in the middle of the pandemic and simultaneously on Disney+.

Disney’s (via ownership of Marvel) Black Panther: Wakanda Forever topped the North American box office with $64 million for the five-day long weekend, taking its total to $367.7 million domestically and $675.6 million worldwide. Fortunately, Disney can be assured that Avatar: The Way of Water to debut in mid-December, will bring in a big tally. More generally, other streamers like Netflix, Warner Bros. Discovery and Paramount Global were lower in late afternoon trading.

Univar Solutions, a specialty-chemicals distributor gained on confirmation that German company Brenntag is in preliminary discussions over a possible takeover of the business.

On sector performance and real estate, basic materials, technology, and energy were leading the way to the downside.

Interestingly on energy, American authorities said they would allow Chevron to resume pumping oil from Venezuelan oil fields, with this likely to lead other oil companies to resume business in Venezuela. Despite this Chevron was modestly lower late afternoon and the energy service giants Halliburton and Schlumberger were little changed.

Gold prices dipped, dragging on exposures like Hecla Mining, Coeur Mining, Harmony Gold and the ETFMG Prime Junior Silvers Miners ETF among others.

The Sprott Physical Uranium Trust declined, and the Invesco DB Agriculture Fund was little changed. Elsewhere, trading was tilted to the downside. Top S&P 500 gainers like Catalent, Wynn Resorts, Ulta Beauty, Activision Blizzard and Las Vegas Sands were mostly modest gainers. Losers were broad-based, including Genius Sports, James Hardie, Vail Resorts, Airbnb, Uber and many others.

Turning to Australia, the ASX200 was down 0.42% to 7229. The sectors leading the gains were Communication Services (+0.62%), Real Estate (+0.54%) and Industrials (+0.33%). The worst performing sectors were Energy (-1.68%), Materials (-0.91%) and Consumer Discretionary (-0.72%). The SPI futures this morning point to a flat open later this morning but with a positive bias.

The Australian mortgage market has a much higher sensitivity to loan rollover than the US market where most homeowners have locked in rates for up to 30 years. The RBA has estimated that 23% of all home loans worth circa $500 billion are fixed rate that will rollover and switch to variable rates by the end of 2023. At the current cash rate, most fixed-rate borrowers with loans expiring in 2023 will see their mortgage rates increase to 3% to 4% when rolling over to variable rates.

With money markets now pricing the RBA cash rate to increase to 3.75% next year, circa 60% of fixed-rate loan borrowers are set to see their minimum payments increase by 40%. This is the interest rate shock that was never meant to happen and was certainly not foreseen by APRA. I see more pain ahead for the residential housing market, particularly among those who are going to have trouble servicing these loans.

Before October 2021, APRA only required banks to apply a mortgage repayment test that involved using an interest rate that was just 2.5 percentage points above the actual product rate. The RBA has already increased its target cash rate by more the 2.5% hurdle which is set to increase further to a terminal 3.75% next year.

Then on October 2021, APRA pushed up the minimum repayment test buffer for banks to 3%, which was also inadequate to cope with the 350-400 basis point interest rate hikes from the RBA. So, the stress testing of Australia’s mortgage market by APRA and the RBA under extreme conditions (such as we are facing now) falls widely short of the mark.

While APRA was clever enough to front-run the RBA by increasing the minimum repayment test buffer to 3%, they did not anticipate the rapid pace of rate hikes to combat stubborn inflation. On Monday, even RBA Governor Philip Lowe apologised to those who may regret taking out a home loan and indicated that interest rates would remain unchanged until 2024. However, the commentary was conditional on the state of the economy and has likely caused many Australians hardship with monthly mortgage repayments, and there is worse to come.

A key question now weighs on the RBA, which is what magnitude of damage will occur for household balance sheets and disposable income by the soaring cost of borrowing? This is crucial for the outlook given that consumer spending accounts for about 50% of total economic growth.

Based on RBA’s data on residential mortgage-backed securities, more than 52% of all borrowers will see spare cash decline by 20% to more than 100%, assuming the target cash rate hits 3.6%. Spare cash is defined as the income the borrower has left over after meeting mortgage repayments and living costs.

It’s also obvious that some will have spare cash turn negative meaning they are at serious risk of defaulting on their loan repayments. This presages a huge reduction in household spending if the RBA hikes the cash rate to 3.6%, which is slightly below current market expectations.

The large reduction in Aussie households’ spare cash is why the RBA has been reluctant to lift interest rates at the same pace of other central banks such as the Fed. Data out on Monday showed retail sales falling for the first time in 2022. In October, the decline in retail turnover marked the end of 9 consecutive month increases and suggests that cost of living pressures including interest rate rises are starting to weigh on consumer spending.

Given the multi-month lags between the RBA raising its target cash rate and lenders passing through these increases to borrowers, the transmission to actual consumer spending, demand and price pressures will take some time and I think the market is yet to price this in. And it will take more months for these shifts in household behaviour to be evident in the official economic data, which is reported on a lagged monthly or quarterly basis. However, all this points to further material downside in the residential housing market, and I see prices falling across the major cities by a further 10% to 15% next year.

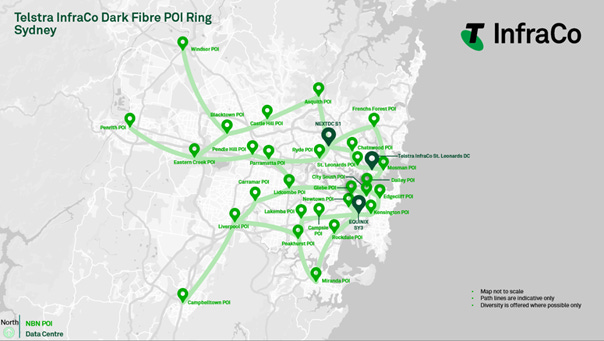

Moving on to stocks, Telstra is attracting interest again as investors are drawn to companies with strong pricing power and market-leading positions. Telstra fits the bill on the front. While competitors such as Optus and TPG are dealing with data privacy and integration challenges, Telstra has a clear opportunity to capitalise on this distraction and incumbent strong subscriber momentum. Telstra also offers an infrastructure-like exposure through the InfraCo assets – particularly the inflation linked receipts from the NBN for use of Telstra’s network assets.

Telco infrastructure assets have been sold on very large multiples in recent years and while there is some risk of valuation pressure given the rise in interest rates, the quality, scale and defensive revenue attributes of Telstra’s network assets make them appealing especially when it is very difficult to find an asset that can be replicated. In my view, Telstra shares still have not captured the upside for the InfraCo assets, which could provide insulation to a market downturn next year when earnings downgrades come through for the broader market.

Telstra also carries less debt relative to earnings, so when the company sells down InfraCo, shareholders would enjoy positive returns through capital management initiatives. We hold shares in the Fat Prophets Global Contrarian Fund, Fat Prophets High Conviction ETF and the Managed Accounts.

On the five-year weekly chart below, Telstra has formed a strong base of support at the $3.80 level and is presently testing resistance at the $4 mark. The multi-month consolidation looks close to being complete and an upward breakout would confirm a return of topside momentum

Bank of Queensland announced CEO George Frazis’ departure with immediate effect, with Chairman Patrick Allaway to take on new responsibilities as executive chairman until a new CEO is found. BOQ said it would launch a domestic and global search to replace Mr Frazis.

Mr Allaway painted Mr Frazis’ departure as a shift in BOQ’s strategic focus, arguing it is about having the right skills for the right phase of growth. Frazis was a former Westpac executive with a reputation for delivering growth and came into the role when BOQ was in decline. The former CEO also made a big move with the $1.3 billion acquisition of ME Bank, which helped deliver a $508 million full-year cash profit to BOQ. Mr Allaway now says BOQ’s focus on four core areas of banking execution, rather than growth, which is something George Frazis was great at delivering. It appears that BOQ is now focusing on a strategic tweak, rather than a major shift. We hold shares in the Managed Accounts.

On the ten year monthly chart below, BOQ remains confined below the primary downtrend but the shares are finding support above $6.50. A breakout however is yet to ensue which points to further sideways consolidation in the months ahead

Turning to Asia, the CSI300 index tracking large caps listed in Shanghai and Shenzhen declined 1.13% while the Hong Kong benchmark fell 1.57%. Stocks trimmed earlier steeper losses to finish well above intra-day lows. While there was some economic data released over the weekend and authorities have ramped up pledges to support the struggling Chinese economy of late, the key driver of negative sentiment was the protests emerging across China (even in Beijing) against zero Covid policy. The scale has been such many are worried about a major crackdown from authorities in response. How Beijing chose to respond in Hong Kong comes to mind.

Besides stocks falling, the yuan weakened against the dollar, with Friday’s announcement by the central bank to cut the required reserve ratio (RRR) for banks by 25 basis points adding to the pressure.

Daily new cases have now pushed above 40,000, prompting more curbs on movements and businesses across the country. Goldman Sachs chief China economist Hui Shan reportedly placed a 30% probability of China reopening before the second quarter in 2023, which “includes some chance of a forced and disorderly exit.”

“The central government may soon need to choose between more lockdowns and more COVID outbreaks,” Reuters reported. Calls for China to tilt its strategy and focus resources on severe cases and improving vaccination among vulnerable groups is rising. After all, most new cases are asymptomatic. China’s healthcare system has relatively low availability of intensive care beds compared to many other countries. The ratio is just 4.53 per 100,000 people and it varies widely across provinces with the ratio typically lower outside the wealthier cities like Beijing and Shanghai. Even that ratio estimate is one of the higher ones I have seen in my research.

To recap the data released over the weekend, profits earned by China’s large industrial firms declined by 3% yoy to 69.78 trillion yuan in the first ten months of 2022. The decline accelerating from the 2.3% drop the prior period as more cities began imposing strict curbs and the property sector liquidity crisis dragging on, dampening consumption.

In Hong Kong trading, the Macau casino operators were the standout, surging as the incumbent licensees were given provisional new 10-year gaming concessions beginning from January. A key detail lacking was how much the companies will need to provide in operating capital for non-gaming business over the life of the concession. Nonetheless, the relief was palpable for the concession holders with US parents. Sands China (+8.4%), MGM China (+13.1%) and Wynn Macau (+15.1%) led the way north for the casino operators.

Wynn Macau is pressuring near-term topside resistance and an important bottom looks to be in. However, until there is a clear line of sight through to China reopening, Macau gaming revenues are going to remain under pressure. An upside breakout above the primary downtrend therefore is not likely for at least a few more months yet

Brewer Budweiser APAC and food delivery platform Meituan logged gains of 2.5% and 2.0% respectively, with both having shown a decent ability to adapt to the restrictions imposed across the country to date. Recent results from Meituan showed the company bouncing back to profit in the third quarter. KFC/Pizza Hut operator Yum China (-0.1%) has also managed better than expected in terms of its financial results, despite in-store dining facing stiff headwinds.

Tech in general faced selling pressure on Monday, with Alibaba (-3.4%) and Baidu (-2.6%) taking a knock, while Tencent Holdings slipped 1.1%. Property developers have been a yo-yo of late, up and down on the various pledges to support the sector, before optimism has faded. On Monday, they were back in the red, with Country Garden Services (-10.8%), Country Garden Holdings (-5.8%) and Longfor Group (-5%) the biggest losers on the Hang Seng.

Elsewhere, local bourse operator Hong Kong Exchanges and Clearing slipped 3%, China Oilfield Services declined 2.1% and gold miner Zhaojin inched 0.1% lower.

In Japan, the Nikkei and Topix declined 0.42% and 0.68% on Monday on jitters about China’s growing Covid cases and protests and uncertainty about how local authorities will respond. There were no major local economic releases in Japan, with retail sales data due today and industrial production on Wednesday. The yen firmed a little, which was another headwind for Japan’s many exporters.

There was an absence of major corporate news, as Japan’s reporting season enters a lull. Risk-off sentiment prevailed and weighed on tech and growth, while the firmer yen dented exporters. Cyber Agent slid 7.6% after Japan lost to Costa Rica in their latest World Cup game over the weekend. The internet company has been streaming the games to Japan fans for free.

The steel sector was a steep faller, with Nippon Steel, JFE Holdings and Kobe Steel all more than 3% lower and among the biggest fallers on the Nikkei. At the other end of the spectrum, investors nibbled away at railway shares, which are set to benefit from Japan’s border reopening. Central Japan Railway (0.7%) and Keisei Electric Railway (0.8%) crept higher, as did defensive names like utilities, with Tokyo Electric Power adding 1%.

Financials were on the back foot on some profit taking after a decent advance in recent weeks. I continue to like the risk-to-reward skew for the sector, with a positive change on yield curve control likely on the agenda in the first half of next year and still ‘super cheap’ valuations. That was not helping them Monday however, with Fukuoka Financial, Chiba Bank and Sumitomo Mitsui Financial all falling more than 2%, while Mebuki Financial, Resona Holdings and Concordia fell more than 1%.

Industrials were mixed with touch screen sensor firm Nissha Co (1.3%) and air-conditioning giant Daikin Industries (0.2%) and component maker THK Co (0.1%) advancing, robotics expert Yaskawa Electric flat, while Apple supplier Alps Alpine (-0.7%) endured a modest decline.

The video games cluster of Sony (-0.8%), Nintendo (-0.9%) and Square Enix (0.2%) were also mixed. Elsewhere, food ingredient firm Ajinomoto edged higher and oil & gas producer Inpex slipped 2.3%.

Major oil & gas producer Inpex is consolidating within a triangle pattern, but above major historic support. The ¥1500 level looks to hold up, and I anticipate a topside breakout and resumption of the upward trend once a bottom is confirmed in global crude markets

The FTSE 100 declined 0.17% and the FTSE 250 slipped 1.30% on Monday, with global markets pressured by protests in China. While there is a possibility this will prompt a quicker move away from zero covid there is also a significant risk the government will double down. Certainly, this is the biggest test to Xi Jinping’s leadership yet and he typically tolerates no dissent.

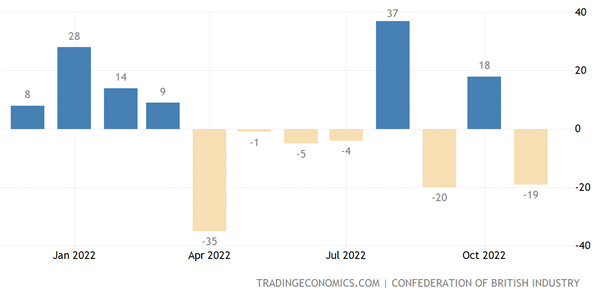

On the domestic data front, the Confederation for British Industry (CBI) distributive trades survey’s retail sales balance in the UK plunged 37 points to -19 in November, indicating a sharp decline in sales. Negatively, firms were anticipating another sales decline next month. The gloomy mood for retailers was set to persist for the next three months, with employment declining for the first time since August 2021 and investment plans deteriorated the most since May 2020. Selling prices surged in the year to November, only a tad below the 37-year record high seen in the prior quarterly survey.

Martin Sartorius, principal economist at the CBI, said, “Retailers and wholesalers contribute £352bn to the UK economy and support a fifth of the nation’s jobs – yet these survey results underline what a tough time it is for the sector. The Chancellor’s decision to back CBI calls for a freeze in business rates next April will provide some welcome relief, but retailers are also looking for longer-term measures from the Government that can restore momentum to the UK economy. Businesses stand ready to work with Government to implement a serious plan for growth that can lift us all out of the current crisis.”

Online property platform Zoopla had some grim news about the UK housing market, saying demand has plunged and homeowners are generally being forced to accept prices below asking. According to Zoopla, buyer demand tumbled 44% year-on-year in the four weeks to November 20 and new property sales declined 28%. Meanwhile, inventories of homes for sale have increased 40% during the same period, although that is still about 20% below pre-pandemic levels.

Zoopla pinned much of the blame on these negative trends on the chaotic mini-budget back in September that saw mortgage rates spike and more mortgage products removed from the market at the time. The agreed sale prices for homes came in about 3% below asking prices, whereas previously owners were receiving their asking price. Zoopla’s Executive Director for Research, Richard Donnell, told Bloomberg he expects the discount to widen on soft demand, and is forecasting UK property prices to fall by around 5% in 2023.

Richard Donnell said, “The housing market is adjusting to a reset in the level of mortgage rates but the likelihood of double digit house price falls at a UK level remains low.”

“While the outlook for house prices is weak, we see a shift to more needs-driven motivations to move in 2023 and beyond which will support sales volumes. Ongoing pandemic impacts, increased labour market flexibility plus more retirement will continue to encourage moves. Cost of living pressures will compound these trends encouraging homeowners to consider their next move.”

Homebuilders were under pressure on the read-across. Persimmon slipped 3.7% and took an extra hit from UBS shifting its rating to sell from neutral. Taylor Wimpey, Barratt Developments and Berkeley Group were 1.8% to 1.9%.

BT Group declined 2.4% after announcing a planned pay rise to much of its workforce, to resolve a dispute with unions. The Communication Workers Union and Prospect have seen both unions recommending its members accept the terms, which are for pay rises of 6% to 16%. There was also a report that BT is considering merging the Global Services division with the Enterprise business to cut costs.

BT Group has underperformed this year, but now looks to be forming an important bottom, which is above the big low of 2020. However, a breakout above topside resistance at the 130p level is required to confirm an inflection is in place

Superdry slid 17.2% despite confirming discussions with a US hedge fund, Bantry Bay Capital, backed by giant Elliott Advisors, to secure a new lender. The faux-Japanese brand warned last month of “material uncertainty” about the future of its business as a £70 million loan facility will expire in January. We do not hold or recommend the shares.

China’s cloudy outlook weighed on oil prices, leading to declines for BP (-1%) and Shell (-0.3%). Small cap waste-to-energy firm Powerhouse Energy slipped 2.7%. Miners BHP (-0.3%), Rio Tinto (-0.3%) and Glencore (0.8%) were mixed. Precious metals miner Fresnillo dipped 1.4%.

In the travel and leisure group stocks were tilted to the downside, although a couple crept higher. Cruise ship operator Carnival (-2.8%), British Airways owner IAG (0.1%) and budget airline easyJet (-2.9%) were mixed. Travel location café and restaurant operator SSP Group (-1.5%) was lower and staycation beneficiary PPHE Hotels added 0.4%.

Elsewhere, defensives were among the better performers. Reckitt Benckiser (1.2%), Unilever (1%), Diageo (0.6%) and RELX (0.5%) advanced. Domino’s Pizza declined 0.7%, online classified leaders Auto Trader (-1%) and Rightmove (-0.4%) were modestly lower. We hold BT Group, PPHE, Fresnillo, Carnival, Powerhouse, Rightmove, Auto Trader, Micro Focus, Domino’s, Shell, SSP Group, Rio Tinto, and BHP. The research team covers those along with BP, IAG, easyJet, Glencore, Reckitt Benckiser, Unilever, Diageo, RELX.

On the continent, loans to households in the Eurozone increased by 4.2% year-on-year in October to €6.81 trillion, slowing from the 4.4% pace in September and compared to the 4.6% pace in May, a 14-year high. Meanwhile, loans to companies increased 8.9% to €5.15 trillion, matching the pace in September, which was the highest since early 2009. Private sector credit growth slowed to 6.5% in October from 7% in September.

The broad M3 money supply in the Eurozone increased 5.1% annually to €16.14 trillion in October, slowing notably from the 6.3% pace in September and below expectations of 6.2% as interest rates rise and recession looms.

European stocks fell on Monday as investors worried about spreading protests in China and the implications for social unrest and hurting the economy. At the close the pan-European Stoxx 50 was down 0.68%, Germany’s DAX fell 1.09% and France’s CAC-40 retreated 0.70%. Italy’s FTSE MIB slipped 1.12% and Spain’s IBEX 35 was in the red to the tune of 1.11%.

Carpe Diem!

Angus

Disclosure: Interests associated with Fat Prophets hold shares in Apple, Alphabet, Disney, Wynn Resorts, Genius Sports, James Hardie, Vail Resorts, Airbnb, Uber, Halliburton, Schlumberger, Hecla Mining, Coeur Mining, Harmony Gold, Global X Silver Miners, Sprott Physical Uranium Trust, Invesco DB Agriculture Fund, Alibaba, Baidu, Tencent Holdings, Yum China, Budweiser APAC, China Oilfield Services, Zhaojin Mining, Hong Kong Exchange and Clearing, MGM China, Sands China, Wynn Macau, Sony, Nintendo, Square Enix, Daikin, THK Co, Nissha Co, Yaskawa Electric, Sumitomo Mitsui, Resona Holdings, Mebuki Financial, Nomura, Chiba Bank, Concordia, Inpex, BT Group, PPHE Hotels, Fresnillo, Carnival, Powerhouse Energy, Rightmove, Auto Trader, Domino’s Pizza, Shell, SSP Group, Rio Tinto, BHP, Telstra, Bank of Queensland, Fat Prophets High Conviction ETF and Fat Prophets Global Contrarian Fund.