Getting more serious

Getting more serious

Key themes and stocks discussed today:

US benchmarks rallied on Tuesday with the help of solid earnings results and good numbers from Microsoft and Visa, which reported after the close. On the other hand, Alphabet disappointed the market and was down sharply in the aftermarket. Higher follow-through in the indexes is expected tomorrow. Bond markets continued to stabilise at the long end. A higher dollar saw oil prices retreat while gold held steady.

Economist David Rosenberg sees similarities between the 2007 cycle and today, with many not prepared for a recession and seeing this as having a low probability. Rosenberg sees complacency amongst investors then and now as one factor to be wary of, ahead of what he sees as a looming recession due to hit in the 1st or 2nd quarter of next year. Paul Tudor Jones, Bill Gross, and several other key players see a high chance of this outcome.

The whisper number on 3rd quarter GDP for the US is that it comes in at 4.8%, however, the consensus is for 4th and 1st quarter growth next year to fall away sharply.

Maybe not firing the bazooka, but China is “getting much more serious” and preparing to intensify efforts to boost and shore up the domestic economy. A report from Reuters said that the government was planning a US$165 billion stimulus.

This fiscal package contrasts with the US$550 spent during the GFC. Cumulative measures are beginning to really add up, which should underpin growth of around 5% into next year. President Xi visited the central bank for the first time since 2008. The Nasdaq Golden Dragon index lifted 4% after investors dumped stocks again yesterday.

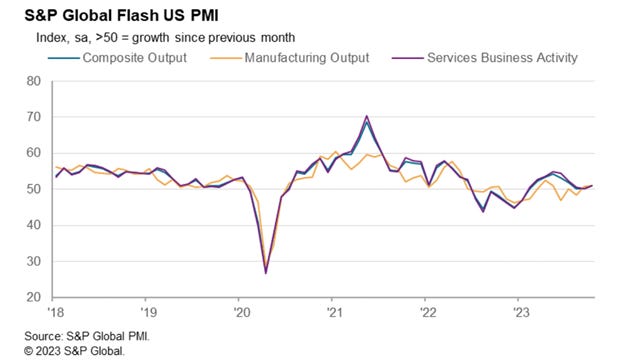

American economic data was supportive, with manufacturing and services activity improvements.

Australian economic data underwhelmed. Manufacturing woes continued, and services dipped back into contraction. RBA Governor Michele Bullock struck a hawkish tone in a speech on Tuesday evening, signalling the RBA won’t sit on the fence should the inflation outlook materially worsen. Fingers crossed for the data due this morning.

Greater China stocks diverged, but we are close to capitulation in the market. Outbound flows and selling by foreigners look close to exhaustion.

UK data was underwhelming, but this should see the BOE stay on the side-lines with rate hikes. The ECB is likely to do the same at this week’s meeting after some woeful manufacturing numbers.

Notable charts and stock mentions include S&P500, Russell 2000 Small/midcap Index, US10yr, WTI crude oil, US dollar index, Nasdaq Golden Dragon Index, Euro STOXX50 index, Oil and geo tensions in the 1970s, Coca-Cola, Spotify, GE, Verizon, Taiwan Semiconductor, Zhaojin, Shiseido, Nidec, Barclays, Rio Tinto, Ansell & CSL.

Good morning,

Wall Street advanced higher on Tuesday as a spate of solid corporate earnings and upbeat forecasts a broad rally. All the major benchmarks lifted, prompted by strong profit results and upbeat guidance from Coca-Cola, GE, and Verizon. Long-dated bond yields continued to settle down following the recent spike above 5%. China announced a much bigger stimulus package to shore up the economy from an ailing domestic property market. The Nasdaq Golden Dragon index jumped 4.5%.

The Dow Jones rose +0.62%, the S&P 500 gained +0.73% to 4,247, and the Nasdaq Composite added +0.93%. The Russell 2000 added +0.82% but remains below important support after a downside break last week. More on this below. The third quarter earnings season has shifted into high gear this week, with around a third of the companies in the S&P 500 reporting results. Of the 118 that have reported so far, 81% have beaten analysts’ expectations, although future guidance and downward revisions have disappointed. The VIX was down 6.5% to 19. After the bell, Microsoft reported an earnings beat, with the shares +4.5% in the aftermarket. Visa also delivered a beat and a $25 billion buyback. Alphabet missed expectations, with the stock down nearly 4% in the aftermarket.

After the worst run since March, the S&P500 has bounced off key support at the primary uptrend (from the October lows) and the 200-day moving average. Scope is raised for further upside extension in the coming days. However, resistance is going to be heavy between the 4300 and 4400 levels being the 50-day moving average and intermediary downtrend. A breakout above 4450 would signal the resumption of upward momentum, however, this is for the SPX to prove with future earnings revisions skewing to the downside for the broader market.

The Russell 2000 Small/Midcap index, after breaking below support at the 1720 level has fallen to 1680, which defines more important historical support. For now, the RUT is managing to hold above the 1680 level, but with the death cross of the 50-day moving average below the 200-day, pressure is mounting for a downside break. This scenario would point to a growing deterioration of the broader market in the US, which is also evidenced by the poor performance of the S&P500 Equal weighted index, which focuses on the breadth of companies as opposed to market weight by capitalisation.

The bond market was more settled at the long end, with the US 10yr and 30yr easing 2 to 5 bps to 4.82% and 4.95%. The short end bucked the trend with the 2yr adding 6 bps to 5.11%. The dollar reversed to the topside, with the DXY rising 0.73% to 106.27, with the euro the worst-faring of the major currencies. Oil prices continued to ease as the market priced in lower perceived geopolitical risks and a more contained war in the ME. WTI and Brent were lower by 2% to $83.66 and $88. Gold and the PGMs were steady. Bitcoin accelerated higher past $35,000.

The US dollar index is threatening the uptrend from the July lows, but Tuesday’s upward dynamic reduced the risk of a downside break below the 105.5 level. The greenback is once again probing resistance above 106.30, and a topside breakout would mark the resumption of the upward trend. A lot is going to come down to where the bond market goes. The US yield curve is higher than most other developed markets and presently enjoys a positive differential, which is attracting global capital flows. This, however could change.

This week, we have important economic data that will be influential on the financial markets and bond yields. On Thursday, the Commerce Department is due to release its first estimate on third-quarter GDP, which consensus forecasts are for a big acceleration to 4.3% from 2.1% last second quarter. The whisper number in the markets is that this could top 4.8%.

This would normally be a great outcome, but for the tumultuous bond market performance, which might react badly. However, the big acceleration in 3rd quarter GDP needs to be held in perspective. Consensus estimates see a decline in GDP growth to around 1% in the 4th quarter. This is one of the reasons why there have been so many downward earnings revisions to earnings estimates in the coming December and March quarters.

One question that investors will be focused on this week is whether the Fed can thread the needle on inflation. This week’s key PCE inflation gauge will provide a window into whether inflation is maintaining a downward trend. If evidence comes through of another big decline, then this will be another factor that stabilises the bond market and would also add conviction to my view that the medium-term highs are now in for the US 10-year yield.

The US 10-year yield has potentially put in an important medium-term top with the recent spike above 5%. Bond bears such as Bill Ackman and Bill Gross have notably pivoted in recent weeks.

WTI crude erased gains this week on the delayed Gaza invasion and global growth concerns. Bearish sentiment might prove fleeting. China launched a big stimulus package aimed at shoring up the economy and property market. Whilst Israel has delayed the invasion into Gaza, the Middle East conflict could quickly escalate. WTI crude has corrected this month but remains comfortable above key support on the two-year weekly chart below. Support looks to be formidable below the $83 level, which should drive a rebound.

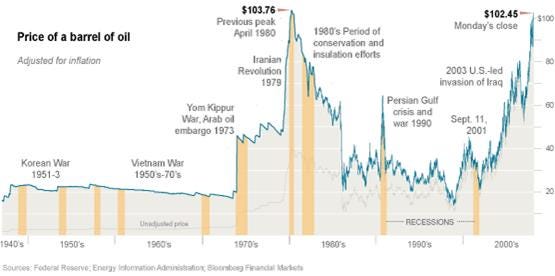

The market has been quick to remove the premium for the outbreak of conflict in the Middle East. This is likely premature given what happened to oil prices during the 1970s when conflict & wars erupted in the ME, and OPEC cutbacks spiked energy prices higher by multiples.

China’s government has approved more fiscal stimulus funded by additional sovereign debt and a boost to this year’s state budget. These efforts will drive more stimulus to shore up the strained economy. The plan details have not yet been made public, but Reuters reported that China is set to approve around $137 billion in sovereign debt issuance. The Nasdaq Golden Dragon Index jumped 4% and has moved off key support. Much more price action on the upside is needed to confirm an inflection, with a breakout and follow-through above 7000, a minimum requirement.

Government advisors are pushing for China to increase the 2024 budget deficit beyond the usual 3% of GDP. This is rational, given the undermining of the economy transmitted by the ailing property market. Beijing has rarely modified budgets mid-year. Previous instances have only occurred in periods of strain, such as the 2008 crash and the 1990s Asian financial crisis. So, it is interesting that President Xi now seems to be pivoting and waking up to the fact that more needs to be done to stabilise the economy.

Beijing has considerable firepower at its exposure to drive a recovery in the economy. The central government’s debt-to-GDP ratio is just 21%, which is much lower than most developed nations. While economists would point to large local government indebtedness with a ratio of 76%, this is also manageable. The US is approaching 121% by way of comparison. In summary, Beijing has considerable resources at its disposal to drive a rebound in the property market and stabilise the economy, which adds to the case that the stock market is in the process of bottoming out.

Highly regarded economist David Rosenberg said that most of Wall Street now anticipates a soft landing with the Fed winning the battle to contain inflation without tanking the economy or causing unemployment to spike. He highlighted in a note this week that there was a similar mood in 2007, when “the consensus and many market participants mistakenly assumed the recession would never come. There are several parallels between the two periods, which underscores why there is potential trouble ahead”.

Mr Rosenberg cited concerns over stock and house valuations being “pricier today relative to incomes and profits than at the peak of the mid-2000s bubbles. Credit-card and auto-loan delinquencies were on the rise, and there were dangerous amounts of debt in the shadow banking sector. The collapse of New Century Financial and Bear Stearns in 2007 were shrugged off as isolated and contained incidents — similar to how the flurry of bank failures this spring is widely viewed. And the current strength of several economic indicators could be misleading”.

David Rosenberg is the former chief North American economist at Merrill Lynch, but he might be misplaced in likening the cycle to 2007 on one front. The GFC was a defining event for a number of generations, myself included. The US housing bubble is nowhere as inflated as it was, and the banking sector is much more regulated. But he makes a point in the cycle amid widespread apathy that a downturn will never arrive.

Mr David Rosenberg

Back in 2007, investors fell “hook, line, and sinker” for the narrative that the boom-bust cycle was history and a “new era” was underway. History is repeating itself, and the US economy is headed for a slump that most people didn’t see coming. I am willing to acknowledge that the recession has been delayed. But it has not been derailed. This recession will come in the next few quarters, not the next few years. “ Rosenberg believes that a surge in job losses and loan defaults is coming, along with faster disinflation, and a new bull market in Treasurys.

Local economic data was supportive,

with the flash reading showing the S&P Global Manufacturing PMI inching higher to 50 in October from 49.8 in September, topping expectations of 49.5. That marked the highest reading in six months, indicating a stabilisation in the sector.

The Services PMI edged upward to 50.9 from 50.1 a month earlier, topping forecasts for a print of 49.8 and in expansion territory. Employment strengthened, and price pressures moderated. Accordingly, the composite PMI rose to 51, a 3-month high and indicating expansion in the private sector.

The PCE deflator, personal spending and income, along with the closely watched University of Michigan consumer sentiment survey, are due later this week.

Mega-caps gained, as the 10-year Treasury yield was fairly stable (down a smidgen at the close) and ahead of Alphabet and Microsoft reporting after the closing bell. I will dive into these results in tomorrow’s correspondence. Most of the group gained +1% to 2%, although Meta was a tad lower, and Apple and Microsoft posted only small advances.

Market bellwether Coca-Cola fizzed higher after a beat-and-raise quarter. Consumers continue to purchase the company’s products despite recent price increases. Organic revenue delivered an impressive 11% growth, while adjusted sales were up 8% at $11.9 billion, above the $11.4 billion consensus. As with other US-based multinationals, the strong greenback is a headwind. Net income attributable to shareholders was $3.09 billion, up from $2.83 billion a year earlier. Adjusted earnings per share of 74 cents surpassed market expectations of 69 cents.

Coca-Cola announced back in July a pause on further price hikes in the US and Europe for the remainder of 2023. Nevertheless, the company’s prices during this quarter were 9% higher than last year’s. Even with these price hikes, unit case volume grew by 2%, outperforming rival PepsiCo. For the full year, Coca-Cola now expects 7% to 8% growth in comparable earnings per share, up from the earlier projection of 5% to 6%. The organic revenue forecast was also revised upward, now anticipating a 10% to 11% increase.

Since breaking below key support on the 2-year weekly chart below, Coca-Cola fell sharply to $52 before rebounding this month. Overhead resistance at the $58.50 level is significant and keeps the stock confined to a trading range.

General Electric (GE) surged after topping expectations and lifting guidance. Total revenues for the quarter hit $17.35 billion, outpacing the consensus estimate of $15.7 billion and marking 20% year-on-year growth. Aerospace revenue jumped 25% to $8.4 billion on surging demand for plane engines and services. The conglomerate began reporting across two segments, with the other, GE Vernova, further divided into Renewable Energy and Power. The Renewable Energy segment posted 15% year-on-year sales growth to $4.15 billion, while the Power segment’s revenues grew by 13% to $3.97 billion. Adjusted earnings of $0.82 smashed the consensus estimate of around $0.56 and more than doubled (+134%) from the previous year.

Verizon surged more than +9% to the top of the S&P 500 after lifting the annual free cash flow forecast. Promotions and a robust 5G network attracted a higher-than-expected number of subscribers in the third quarter.

There is a stream of companies reporting. Briefly on a few, Aerospace firm RTX Corp announced a $10 billion share-buyback program to mitigate the repercussions of internal problems with a key aircraft engine. The shares surged from subdued levels. 3M Co revised full-year earnings forecasts upwards, reflecting strong demand and sending the shares sharply higher.

Spotify Technology surged after third-quarter results exceeded expectations, especially in sales and subscriber growth, even as price hikes were pushed through. Consumer staples firm Kimberly-Clark was slightly lower despite raising the annual earnings outlook. Spotify looks close to completing an inflection higher.

Elsewhere, DraftKings popped on an upgrade by Moffett Nathanson, boosting Genius Sports on the read-across. The surge for Bitcoin over the past week is lifting the likes of leading exchange Coinbase, extending gains again on Tuesday. Oil prices dipped as Israel seems to be holding off on a ground invasion of Gaza for now, resulting in declines for Halliburton and Schlumberger on Tuesday.

Taiwan Semiconductor (+0.6%) looks poised to benefit from Nvidia’s (+1.6%) plans to take on Intel in the CPUs space. The contract manufacturer is the partner of choice, given leading technology and a strong track record in developing new products.

Since Berkshire Hathaway’s emergence on the share register last year triggered a big rebound in Taiwan Semiconductor to highs above $110, the stock has consolidated. On the 5-year weekly chart below, TSM has this year retraced around half the advance to $110, which defines a big resistance level. Support has been found at the $85 level, with TSM tracing out a series of higher lows. The technical setup is encouraging, and a retest of the resistance at $110 should ensue over the coming year.

The ASX200 ticked +0.19% higher, recovering from 11-month lows plumbed on Monday, with six of the eleven sectors finishing in the green. Materials +0.85% and Energy +0.4% logged the most significant gains, while Consumer Staples -1% and Utilities -0.5% were the biggest losses. Investors shrugged off continued volatility in the stock markets. Local data was underwhelming, with manufacturing woes continuing and the services sector reversing into contraction. SPI futures are pointing to a 0.35% gain today.

The Energy sector benefitted from higher oil prices, with heavyweights Santos +0.6% and Ampol +1.2% higher. Viva Energy +4% was a solid gainer, bolstered by positive broker coverage. Materials recouped some of the previous day’s hefty losses, boosted by +1% gains for iron ore with BHP, Rio Tinto and Fortescue advancing +0.5% to +2.6%. Uranium names Paladin Energy +2.2% and Boss Energy +4.6% had a good day. There were some bounces for the battered lithium sector, while coal continued to perform, with Whitehaven Coal +1.2% extending gains and New Hope Corp +2% recovering after going ex-dividend.

On the macro side, RBA Governor Michele Bullock struck a hawkish note in a speech on Tuesday evening, underscoring a commitment to combating inflation and signalling a firm stance despite the burden to borrowers. Like her predecessor before her, this is the right approach to avoid more significant economic problems down the road.

Ms Bullock said, “The Board will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation. At the same time, the Board is mindful that growth in demand and the rate of inflation have been moderating, and that there are long lags in the transmission of monetary policy.” The walk on the tightrope for Australia is set to continue for some time, particularly with inflation still elevated.

Her speech echoed the tone we saw in the RBA minutes from the last meeting. Ms Bullock ruled out the RBA linking specific employment metrics to policy, with the focus on bringing inflation back to the 2-3% target. Responding to the hawkish tone, bond markets are now forecasting an additional 25bp hike in the coming six months before cuts later next year.

Currently, the RBA seeks to maintain low inflation and full employment. Unlike the inflation band, specifically defined as 2-3%, full employment isn’t as tightly defined. “While inflation, appropriately, has a numerical target, it would be unwise to specify a fixed numerical target for full employment. For one, full employment can change over time, as the structure of our economy evolves. It is also not a concept that can be directly measured. And it cannot be comprehensively summarised by a single statistic such as the unemployment rate.”

The speech came on the cusp of the Australian CPI data due today while following local manufacturing and services PMIs. The Judo Bank Flash Australia Manufacturing PMI fell to 48 in October, from 48.7 in September, and narrowly missed expectations after being in contraction for eight straight months.

The Services PMI was more disappointing, falling to 47.6 in October from 51.8 in the prior month, well below expectations. Together, these indicated a month of contraction in the private sector, with most damage coming from the steep fall in services activity. Australian consumers are unquestionably reining in spending as economic conditions become tougher.

CSL added +0.19% and is stabilising after holding an investor day, which outlined strong growth plans for Australia’s largest healthcare company. CSL has fallen sharply on concerns that Novo Nordisk’s Ozempic weight loss drug has shown early signs of success in delaying the progression of kidney disease in diabetes patients. This could potentially impact the value of subsidiary Vifor’s kidney disease business. Vifor was acquired last year. We remain confident in the outlook for CSL, and this is a view shared by investment banks Citi, UBS, JP Morgan and Morgan Stanley.

The large multi-year triangle range pattern that CSL had been forming for a number of years on the 10-year monthly chart below has not worked out. Since breaking below key support at the uptrend, CSL fell sharply to also take out the $260/270 level, which defined the lower end of a multi-year range.

CSL has since fallen sharply. Support, however, looks to have been found at $230, being the breakout level back in 2018. Resistance at the $260/270 should cap CSL near term, but support is formidable below $230 and should drive a recovery next year. A break below the $230 level would be negative and raise the scope for further downside, however, this is not the technical base case.

Medical glove and surgical suits maker Ansell -1.2% held their AGM yesterday, where management provided context that trading in FY24 was so far in line with expectations. Supply pressures within the industry were easing back towards normalcy while demand is recovering after the COVID-19 pandemic spike in sales. Management reiterated guidance for EPS to range between US57¢ and US77¢ in FY24.

On the 20-year monthly chart below, Ansell has fallen by over 50% since the pandemic spike in demand for its products. This overshoot now appears to have worked off, with sales and costs normalising after what has been a volatile period for earnings. Ansell has pulled back to the primary uptrend on the 20-year chart below with strong support at the $20/$21 level. Only a breakdown below the primary uptrend at $20 would refute the bullish technical case, which has scope for a broader recovery towards $26/$28 in the coming year.

Materials led the market to the upside yesterday, with notable gainers, including Lynas Rare Earths +12.4%, Pilbara Minerals +5.3%, and IGO +2.9%. Lynas Rare Earths soared +12.4% after an operating license was granted in Malaysia. S&P Dow Jones Indices announced that Newcrest Mining -1.2% will be removed from the ASX200 due to the acquisition by Newmont. Shares in Newcrest will cease trading on the 26th of October, and Newmont CDIs will commence trading on the following day.

Greater China stocks diverged on Tuesday. Chinese stocks experienced a modest uptick on Tuesday, with the CSI300 advancing +0.37%, while the Hang Seng fell -1.05% as trading resumed following a long weekend. The CSI300 picked up slightly from more than 4-year lows as state-fund Central Huijin purchased ETFs in a bid to bolster confidence. Hong Kong and China futures are pointing to gains of 2%/3% following the latest stimulus announcements from Beijing.

In a further sign of capitulation, investors reportedly offloaded another approximately 5 billion yuan ($684.3 million) worth of Chinese shares through Stock Connect, continuing the trend of outflows from Chinese equities. According to a report out on Reuters, China is anticipated to greenlight over 1 trillion yuan in additional sovereign debt to stimulate growth, adding to other measures steadily rolled out over the past year.

Property stocks resumed a dive in Hong Kong, with China Evergrande -8.1%, Country Garden -5.3% and Longfor -4% tumbling. Big tech was another drag, as JD.com and Tencent slipped by more than -2%, Alibaba fell -1.7% Baidu -0.5% and Meituan -0.3% logged more modest losses. At the other end of the spectrum, local bourse operator Hong Kong Exchanges and Clearing +1.7% and gold miner Zhaojin +1.5% posted respectable gains.

Japan’s stock market enjoyed a rebound on Tuesday, albeit in a trading session marked by significant volatility. The Nikkei index snapped a 3-day losing streak and had a big swing intraday to climb +0.2%, while the broader Topix added +0.09%.

Traders took local economic news in stride despite headline readings narrowly undershooting expectations. Japan’s manufacturing sector signalled continued contraction, with flash reading down slightly at 48.5, marking the fifth month of deteriorating conditions. This was attributed to a persistent decline in new orders. In contrast, growing at the slowest pace since last December, the services sector came in at 51.1 in October.

Electric motor maker Nidec tanked -10.5% as, despite reporting increased quarterly earnings, only maintained the annual profit forecast. The steady profit forecast of ¥220 billion for the year to March 2024 fell short of market expectations. The stock was easily the biggest decliner among the Nikkei constituents. Shippers Kawasaki Kisen Kaisha -4.1% and Nippon Yusen -2.6% were the second and fourth biggest fallers, respectively.

Index heavyweights Fast Retailing and SoftBank Group provided substantial support to the Nikkei, both advancing +1.7%. Cosmetics firm Shiseido +3.4% featured as a top gainer and is benefitting from the return of tourism as people flock to Japanese shores, with the weak yen adding to the appeal.

Shiseido is resting on historical support, which should hold. Only a breakout above resistance at the ¥7200, however, would raise the scope for an inflection.

Our video games cluster of Square Enix +2.4%, Sony +1% and Nintendo +0.2% advanced. Banks were in the red, led lower by regionals Chiba Bank -1.9%, Resona Holdings -1.8% and Concordia Financial -1%.

Traders shook off underwhelming local data to bid the FTSE 100 +0.2% higher by the close on Tuesday. A disappointing update from Barclays hit the banks and capped gains. The turning point seemed to come in the afternoon following robust economic data from across the Atlantic and as Gilt yields retreated. The FTSE 250 dipped -0.38%.

The ONS reported an increase in the unemployment rate to 4.2% for the three months ending in August, up from 4.0% in the previous period. These figures were based on a new methodology and are being floated as experimental statistics. As such, there is some uncertainty about how they will be interpreted. The general thinking seemed to be that there is enough slack in the jobs market that the BOE will likely hold rates steady at the next meeting.

Both manufacturing and services activity remained in contraction in October, according to flash estimates.

Among the blue chips, mining giant Rio Tinto +3.5% led the gainers, buoyed by Barclays’ upgrade to ‘overweight’. Other miners, Antofagasta, Anglo American, BHP and Glencore, posted gains of +1.4% to +2.4%. Rate-sensitive stocks benefitted from a retreat in bond yields, with United Utilities, Severn Trent and SSE plc rising +1.9% to +2.6%.

Conversely, Barclays slid -6.5% despite its third-quarter profits surpassing forecasts, as the bank reduced net interest margin guidance for 2023. This led NatWest -3.5% and Lloyds -2% to tumble on the read-across.

Bunzl, the distribution firm, reported a 5% revenue decline for the third quarter, with this attributed to post-pandemic normalisation trends and sending the stock -4% lower.

On the continent, soft regional economic data bolstered investor sentiment, with traders betting the ECB will stand pat on interest rates at the meeting on Thursday. Another factor here is that recent inflation data showed a nice downward trend, reducing pressure on the ECB for the inflation battle, although still well above the desired target.

The flash PMI reading for the Eurozone manufacturing sector continued to be woeful, dipping slightly to 43, a smidgen below expectations, as new orders fell sharply again. The services sector declined to 47.8, missing expectations for a reading of 49.1. The composite PMI unexpectedly dropped to 46.5, the worst reading in 35 months. Excluding pandemic-impacted months, this represents the steepest decline in activity in over a decade.

Meanwhile, consumer sentiment in Germany declined for a third straight month in October, with a headline reading of -28.1.

The major European markets were advanced. At the close, the pan-European Stoxx 50 was up +0.58%, Germany’s DAX gained +0.54%, and France’s CAC-40 advanced by +0.63%. Italy’s FTSE MIB inched +0.05%, while Spain’s IBEX 35 was the odd one out, dipping -0.22%.

Despite poor sentiment and the struggling German economy, the Stoxx 50 index is only 14% down from the record highs, resting on key support at 420. However, further deterioration of the index back to the 400 level (being the primary uptrend) would see the index in bear market territory.

Carpe Diem!

Angus

Disclosure: Fat Prophets and its affiliates, officers, directors, and employees may hold an interest in the securities or other financial products relating to any company or issuer discussed in this report. Fat Prophet’s disclosure of interest related to Investment Recommendations can be provided upon request to members@fatprophets.com.au.